Pay-by-link payments are becoming a fast and simple way for businesses to collect payments globally. In this article, I break down the top US companies offering this service, compare their features, and share practical insights to help you choose the right provider for your business.

Over the last few years, I have seen a clear shift in how businesses accept payments. Earlier, everything depended on checkout pages, POS machines, or manual bank transfers. But now, one simple concept is changing the game — Pay-by-Link payments.

In simple words, pay-by-link allows a business to send a payment link through WhatsApp, email, SMS, or even social media. The customer clicks the link, enters details, and completes the payment instantly. No app download, no complex checkout.

And this is not just a trend. It is becoming a core payment strategy globally.

As per data available from Statista, digital payment transactions are expected to cross $15 trillion globally by 2026, and a big chunk of this growth is coming from flexible payment methods like payment links.

From my experience working with fintech startups and payment platforms, I have noticed three major reasons behind this growth:

- Businesses want faster payment collection

- Customers prefer frictionless checkout

- Global transactions need simple, shareable payment options

Especially in industries like:

- Freelancers & service providers

- Travel businesses

- High-risk industries (adult, gaming, crypto)

- B2B invoice-based payments

Pay-by-link solves a real problem — getting paid quickly without building complex payment flows.

Why US Companies Are Leading This Space

The US market is ahead in adopting flexible payment infrastructure. Based on what I have observed:

- US fintech companies are building API-first payment systems

- They support multi-channel payments (email, SMS, social)

- Strong focus on compliance + fraud prevention

- Easy integration with SaaS, CRM, and invoicing tools

Because of this, many global startups and even Indian businesses prefer using US-based pay-by-link providers.

What You Will Learn in This Article

In this article, I will break down:

- Top 5 US companies offering pay-by-link services

- Their key features and real use cases

- Which type of business should use which platform

- What to consider before choosing a provider

About Make An App Like

At Make An App Like, we work closely with startups and fintech businesses building payment systems, marketplaces, and SaaS platforms. Based on our real project experience, I am sharing insights that actually help in decision-making, not just theory.

If you are a founder, payment startup, or even a service business — this topic directly impacts your revenue flow.

How Pay-by-Link Works (Business + Technical Breakdown)

When I first started working with payment systems, I used to think payment links are just a “shortcut” to checkout. But after building and analyzing multiple fintech solutions, I realized — pay-by-link is actually a full payment infrastructure layer, not just a feature.

Let me break it down in a simple and practical way.

How Pay-by-Link Works (Business Flow)

At the business level, the flow is very straightforward:

- A business creates a payment request (amount + purpose)

- The system generates a unique payment link

- The link is shared with the customer (WhatsApp, email, SMS, etc.)

- Customer clicks the link and lands on a secure payment page

- Payment is completed using card, bank transfer, or wallet

- Business receives confirmation instantly

From my experience, this reduces payment delays by 30–50%, especially in service-based businesses.

Why? Because you are removing friction. No login. No navigation. Just click and pay.

Where It Works Best (Real Use Cases)

I have personally seen pay-by-link working extremely well in these scenarios:

1. Freelancers & Agencies

Instead of sending invoices and waiting for days, you send a link and get paid faster.

2. Travel & Booking Businesses

Customers confirm bookings instantly without going through a long checkout process.

3. High-Risk Industries

In industries like adult, gaming, or crypto, traditional checkout often fails. Payment links act as a flexible alternative.

4. B2B Payments

Sales teams can close deals faster by sending quick payment requests.

5. Social Commerce

Selling through Instagram, WhatsApp, or Telegram becomes easy with direct payment links.

Technical Breakdown (What Happens Behind the Scene)

Now let me explain what actually happens technically — in simple terms.

When a payment link is created:

- A unique transaction ID is generated

- It is mapped to:

- amount

- currency

- merchant account

- A secure hosted payment page is created

Behind the scenes, the system connects with:

- Payment gateways

- Fraud detection systems

- Compliance checks (KYC, AML where needed)

- Settlement systems

Once the customer pays:

- The transaction is processed through the gateway

- Funds are routed to the merchant account

- Status is updated in real-time via API/webhooks

From a developer perspective, most US companies offer:

- REST APIs

- Webhooks for payment status

- SDKs for faster integration

Why It’s Better Than Traditional Checkout

From what I have observed across projects, pay-by-link has some clear advantages:

- No need to build full checkout pages

- Works across all devices instantly

- Faster payment collection cycle

- Easy to integrate with CRM and invoicing tools

- Ideal for global and remote transactions

But at the same time, it’s not perfect.

Limitations You Should Know

- Less control over branding (depends on provider)

- Can feel less “customized” than full checkout

- Requires strong fraud monitoring

- Some providers restrict high-risk industries

That’s why choosing the right provider matters a lot.

Top 5 US Pay-by-Link Payment Companies (Detailed Breakdown)

Now let’s come to the main part.

I am not just listing random companies here. I am selecting these based on:

- Real usage in fintech and SaaS products

- API flexibility

- Support for different business models

- Global usability

- My experience working with similar payment systems

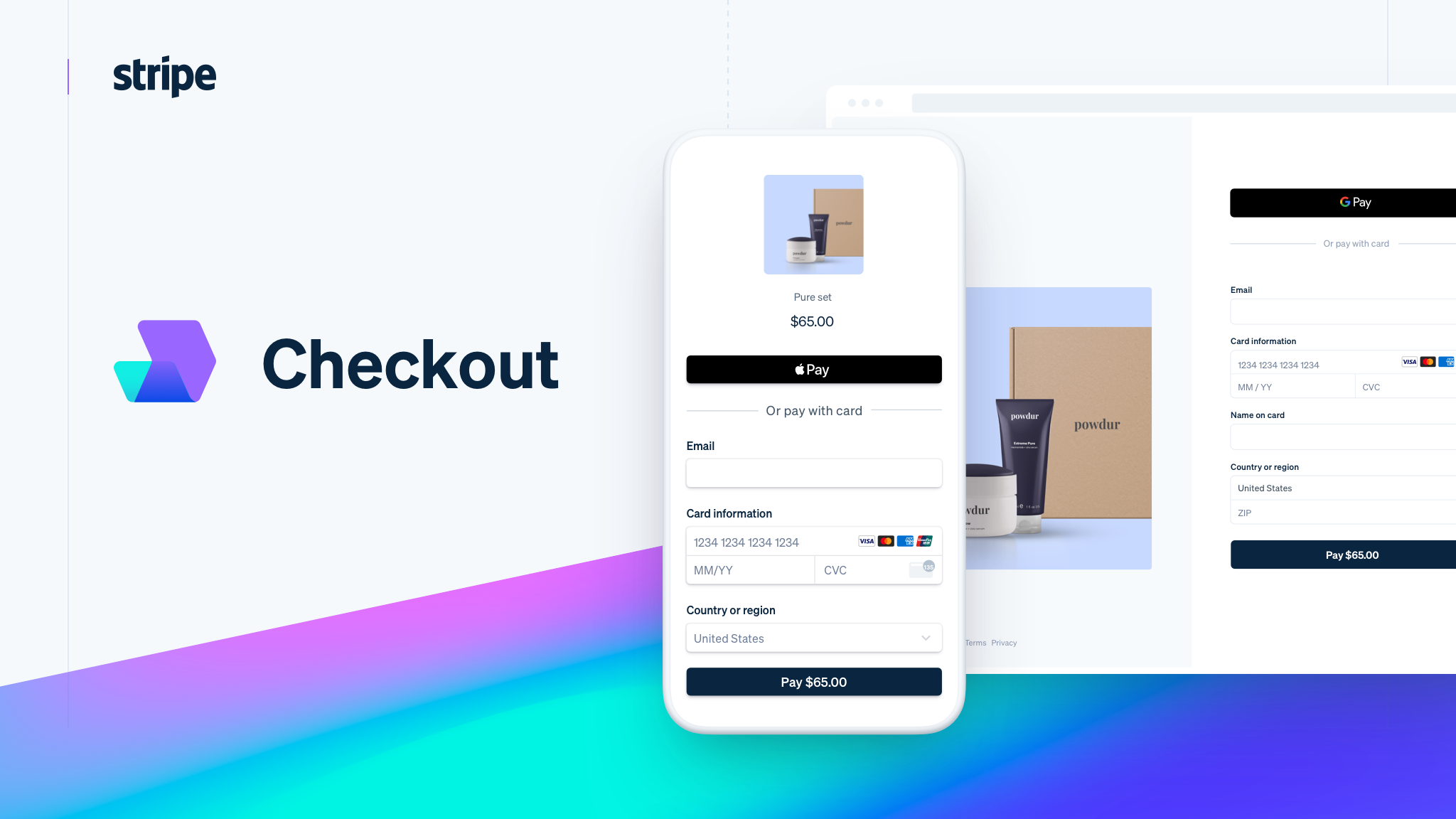

1. Stripe

4

From my experience, Stripe is the most developer-friendly payment company in the world. Their Payment Links product is extremely simple yet powerful.

Best Features:

- Create links without coding

- Supports global payments (cards, wallets)

- Highly customizable checkout

- Strong API ecosystem

Best Use Cases:

- SaaS platforms

- Freelancers & agencies

- Subscription-based businesses

My Insight:

If you are building a product and want full control + scalability, Stripe is usually the first choice.

2. Square

4

Square is known for simplicity. Their pay-by-link feature works very well for small and medium businesses.

Best Features:

- Easy setup without technical knowledge

- Works well with POS + online

- Built-in invoicing + payment links

- Strong US market presence

Best Use Cases:

- Retail businesses

- Local service providers

- Restaurants & offline businesses

My Insight:

If your focus is US customers and you want something simple, Square is very reliable.

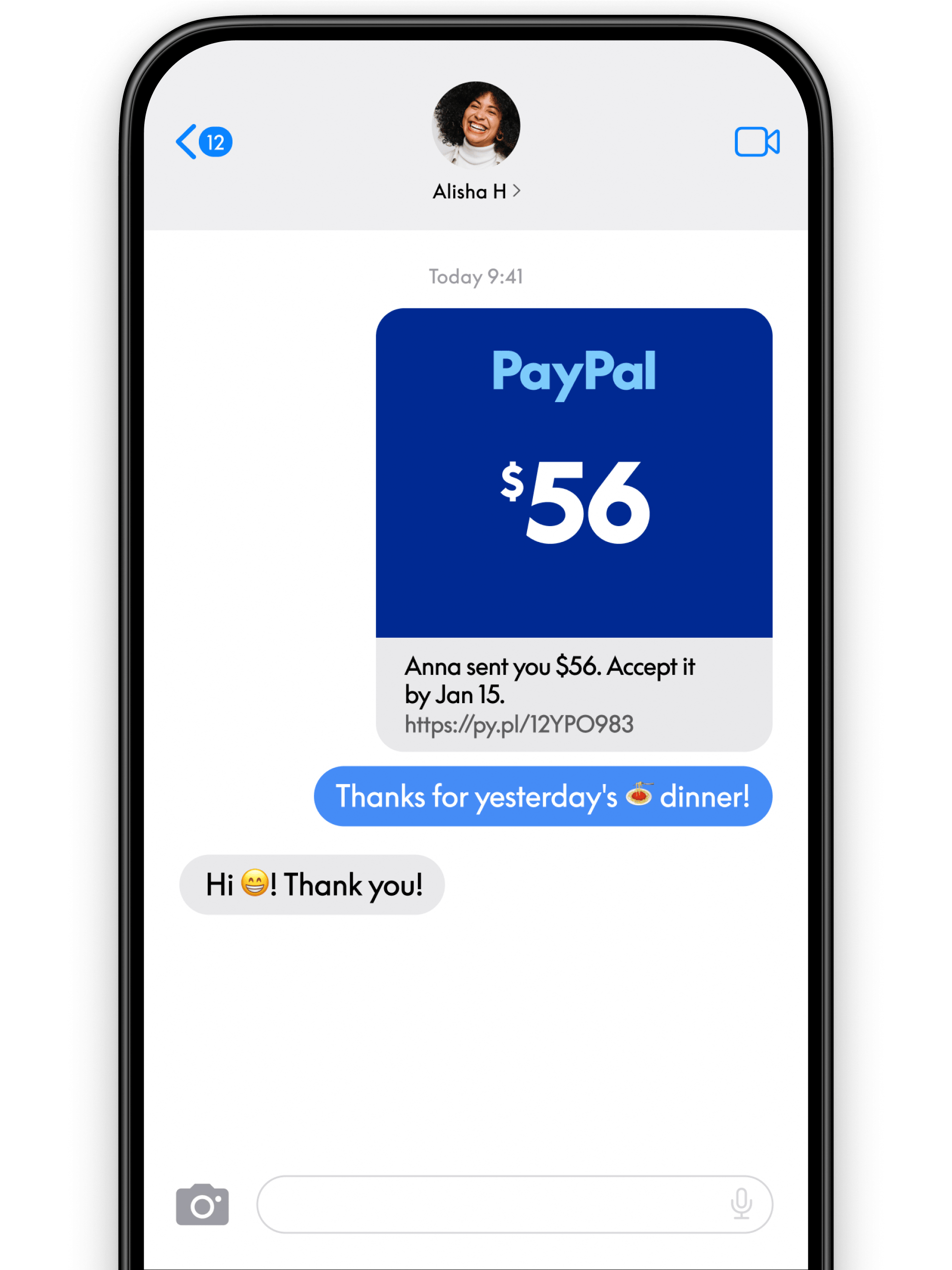

3. PayPal

PayPal is one of the oldest and most trusted payment systems globally. Their PayPal.Me and payment request links are widely used.

Best Features:

- High trust factor among customers

- Works in multiple countries

- Easy payment request links

- Supports wallets and cards

Best Use Cases:

- Cross-border payments

- Freelancers

- Individuals and small businesses

My Insight:

If trust and brand recognition matter for your customers, PayPal gives a strong advantage.

4. Authorize.Net

Authorize.Net is backed by Visa and is more focused on secure and stable payment infrastructure.

Best Features:

- Strong fraud detection tools

- Reliable payment processing

- Supports recurring billing

- Hosted payment forms and links

Best Use Cases:

- Enterprises

- Businesses needing strong compliance

- Subscription-based models

My Insight:

If security and compliance are your priority, this is a solid choice.

5. Helcim

Helcim is not as famous as Stripe or PayPal, but I have seen it growing fast, especially among cost-conscious businesses.

Best Features:

- Transparent pricing

- Payment links + invoicing

- Good customer support

- No long-term contracts

Best Use Cases:

- Small to mid-size businesses

- Businesses focused on cost optimization

My Insight:

If you want lower fees with decent features, Helcim is worth considering.

My Quick Take (From Experience)

If I simplify it based on real usage:

- Stripe → Best for developers & startups

- Square → Best for offline + simple businesses

- PayPal → Best for trust & global payments

- Authorize.Net → Best for compliance-heavy businesses

- Helcim → Best for cost efficiency

Feature & Pricing Comparison (Copy-Paste Ready)

Now let’s make this practical.

Whenever I help a founder choose a payment provider, I don’t just look at features. I focus on:

- Cost per transaction

- Ease of integration

- Approval rates

- Industry compatibility (especially high-risk)

- Scalability

So instead of long explanations, here is a clear comparison table you can directly use.

Pay-by-Link Providers Comparison Table

| Company | Transaction Fees (Approx) | Pay-by-Link Feature | Best For | Global Support | Key Strength |

|---|---|---|---|---|---|

| Stripe | 2.9% + $0.30 per transaction | Yes (No-code + API) | Startups, SaaS, Developers | Yes | Highly customizable, strong APIs |

| Square | 2.6% + $0.10 per transaction | Yes (Easy setup) | SMBs, Retail | Limited (Mostly US) | Simple and quick onboarding |

| PayPal | 2.9% + fixed fee (varies by country) | Yes (PayPal.Me, Requests) | Freelancers, Global payments | Yes | Strong brand trust |

| Authorize.Net | $25/month + 2.9% + $0.30 | Yes (via invoicing/links) | Enterprises | Yes | High security & fraud tools |

| Helcim | Interchange + small markup (~1.8%–2.5%) | Yes (Invoicing + links) | Cost-focused businesses | Limited (US/Canada) | Transparent pricing |

What Most Founders Miss (My Observation)

From my experience, many founders make one big mistake — they choose based on fees only.

But in reality, these factors matter more:

- A slightly higher fee with better approval rate = more revenue

- Better UX = faster payment completion

- Global support = more customer reach

For example:

- Stripe may look expensive, but its conversion rate is usually higher

- PayPal may have higher fees, but it increases customer trust and checkout completion

Quick Decision Framework (Simple Logic)

If you are confused, use this:

- Building a tech product → Go with Stripe

- Running a local business → Choose Square

- Selling globally → Use PayPal

- Need strong compliance → Use Authorize.Net

- Want lower cost → Consider Helcim

Real Cost Insight (Important)

Based on real implementations I have worked on:

- Average payment processing cost = 2.5% to 3.5% per transaction

- High-risk industries = can go up to 5%–8%

- Cross-border payments = additional 1%–2% FX fees

So always calculate:

Total cost = Processing fee + FX fee + chargeback risk

In the next section, I will explain which platform you should choose based on your business model, with real-world scenarios.

Which Pay-by-Link Provider is Best for Your Business (Use Case Based)

Now this is the most important part.

I have worked with multiple startups and payment integrations, and one thing I can clearly say — there is no single “best” provider. The right choice depends completely on your business model.

So instead of giving generic advice, I will break this down based on real scenarios.

If You Are Building a SaaS or Tech Product

If your product includes subscriptions, recurring billing, or global users, then:

Go with Stripe

Why:

- Easy API integration

- Subscription support built-in

- Webhooks for automation

- Scalable for global growth

My Experience:

In most SaaS projects I have worked on, Stripe reduced development time significantly because everything is already structured.

If You Run a Local Business or Offline Store

If your business is mainly US-based and deals with walk-in or local customers:

Choose Square

Why:

- Very easy setup

- Works with POS + online

- Payment links + invoicing in one system

Best For:

- Salons

- Restaurants

- Local service providers

If You Deal with International Customers

If your customers are from different countries and trust matters:

Use PayPal

Why:

- Globally trusted brand

- Easy cross-border payments

- Customers already familiar with it

My Observation:

In many cases, adding PayPal increased payment success rate because users feel safer.

If You Need Strong Security & Compliance

If your business handles sensitive transactions or needs strict compliance:

Go with Authorize.Net

Why:

- Advanced fraud detection

- Backed by Visa

- Stable infrastructure

Best For:

- Financial services

- Subscription-heavy businesses

- Enterprises

If You Want Lower Fees and Simple Setup

If your focus is saving cost while maintaining decent features:

Conclusion + Future Trends + Final Advice

After working closely with fintech startups, SaaS platforms, and high-risk businesses, one thing is very clear to me — payments are no longer just a backend function. They directly impact your revenue, customer experience, and scalability.

And pay-by-link is becoming a default payment method, not just an optional feature.

What I Have Seen in the Market

Based on my experience and industry data:

- Businesses using simplified payment flows see 20–40% faster payment collection

- Conversion rates improve when checkout friction is reduced

- Customers prefer instant, mobile-friendly payments

As per reports from McKinsey & Company, frictionless payment experiences are one of the top drivers of customer retention in digital businesses.

Future Trends You Should Watch

If you are building or scaling a business, these trends matter:

1. Payments Moving to Conversations

Payments are shifting to WhatsApp, email, chat, and social platforms. Pay-by-link fits perfectly here.

2. Rise of Payment Orchestration

Businesses are no longer depending on a single provider. They use multiple gateways and route transactions smartly.

3. AI in Payment Optimization

Fraud detection, routing, and approval optimization are becoming AI-driven.

4. Growth of High-Risk Payment Solutions

More companies are building specialized infrastructure for adult, gaming, crypto, and similar industries.

Final Advice (From Real Experience)

If I had to summarize everything in a simple way:

- Do not choose a provider based only on fees

- Always think about scalability from day one

- Keep backup payment options ready

- Focus on user experience — it directly affects revenue

And most importantly: